The question this raises is fundamental for anyone studying M&A. Why would a billionaire with the financial capacity to acquire the entire club settle for less than a third of the equity? And why would the Glazers, who had been pushed by fans for nearly two decades to sell, agree to dilute themselves only partially while handing over the part of the business that arguably generates most of the brand value? The answer lies in the way both sides priced risk, control, and optionality.

A premium valuation backed by a strategic thesis

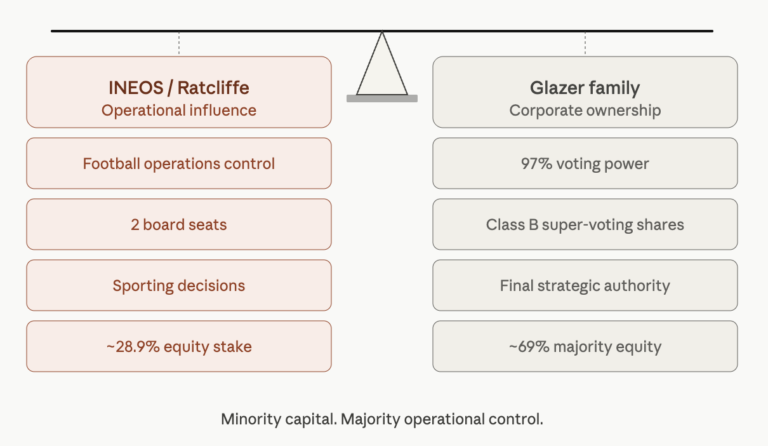

The implied enterprise value of Manchester United at the time of the deal was around 5.2 billion pounds. That figure translated into an EV-to-sales multiple of roughly 9.3 times, which sits noticeably above the 6.0 times average that analysts apply to the rest of the Big Six in the Premier League. In other words, Ratcliffe did not negotiate a discount for being a minority shareholder. He paid a control premium for a non-controlling stake, which is exactly the kind of pricing that finance textbooks tell you to avoid.

There were reasons for that premium, and they made sense in 2023. Manchester United remains one of the strongest sports brands on the planet, with a global fan base, deep commercial reach, and a revenue profile heavily skewed toward high-margin sponsorship and commercial income. The thesis was that the club had been chronically underperforming relative to its commercial potential, and that injecting INEOS-style operational discipline, drawn from the group’s experience in cycling, sailing, and Formula 1, would unlock value that the Glazers had failed to capture. There was also a clear capex angle. Old Trafford had become outdated, and Ratcliffe earmarked an additional 300 million dollars specifically to enable future infrastructure investment, with the longer-term ambition of building what he later called the Wembley of the North.

For Ratcliffe, the premium reflected a bet on three layers of value creation. The brand was undermonetized, the sporting structure was broken and could be fixed, and the stadium project would unlock a new revenue ceiling. For the Glazers, the premium was the only acceptable price to give up operational control while keeping their economic and voting majority intact. Both sides walked away believing they had structured something elegant. The reality has been more complicated.

Two years later, the numbers tell a more complicated story

The most recent valuation work from independent analysts now places Manchester United’s equity value at around 4.2 billion pounds, using a still-generous 8.0 times EV-to-sales multiple that reflects the club’s brand premium relative to peers. That figure is roughly one billion pounds below the implied valuation at which Ratcliffe entered. On paper, his stake has lost value, and the broader market environment has not helped. Manchester City, Liverpool, and Arsenal now generate more commercial revenue than United on a forecast basis for the 2025-26 season, which is a remarkable shift for a club that historically defined the commercial ceiling of English football.

The financial profile of the club has deteriorated in parallel. Net debt has climbed above one billion dollars, the highest level since the Glazer family executed their leveraged buyout in 2005, an event still remembered as a textbook example of how shareholder extraction can weigh on a sports asset for decades. Total football net debt, which includes transfer liabilities, has reached 1.047 billion pounds, roughly 49 million pounds higher than the moment Ratcliffe acquired his stake. The club drew down a record 290 million pounds from its revolving credit facility by December 2025. Despite record revenues of 666.5 million pounds in the financial year ending June 2025, Manchester United posted an overall loss of 33 million pounds, dragged down by missed European qualification and elevated operating costs.

Where the picture becomes more interesting is on the sporting side, because the early signals of recovery are now visible. United currently sit third in the Premier League with 65 points, behind only Arsenal and Manchester City, after enduring one of the worst seasons in their modern history just months earlier. The cost-cutting program INEOS pushed through, with more than 250 redundancies and a wage-to-revenue ratio that fell from 56% to 52.5% within a year, has clearly not crippled performance on the pitch. The quarterly wage bill in the most recent reporting period was the lowest since 2020, which is a meaningful achievement when paired with a top-three league position. From a pure operational efficiency standpoint, the discipline INEOS promised has been delivered, and the sporting trajectory is finally pointing upward.

That partial recovery, however, does not resolve the deeper question raised by the deal. Sporting performance, in elite football, is volatile by nature. One strong season does not justify a one-billion-pound valuation gap, especially when the underlying financial structure remains under pressure and the next major capex commitment has barely been priced into the balance sheet. The Ratcliffe thesis was never about a single season of recovery. It was about durably resetting the commercial and competitive ceiling of the club, and on that longer-horizon test, the verdict is still very much open.

The governance question nobody priced correctly

This is where the structure of the deal starts to show its limits. When everything is going well, the separation between ownership and operational control can work. INEOS handles the football, the Glazers handle the corporate envelope, and both sides align on the broader direction of the club. When things go badly, however, the same structure becomes a source of friction. Who decides whether to invest more in the squad when the club is haemorrhaging cash? Who carries the reputational cost of unpopular decisions, like layoffs or ticket price increases? Who has the final say when sporting ambition collides with financial discipline?

In a traditional acquisition, these questions are resolved by the simple fact that one party owns the asset. In the Manchester United deal, they are resolved through a delicate balance of delegated responsibility, board seats, and informal influence. The current sporting recovery has eased some of the visible pressure on this structure, but it has not removed it. Industry observers have repeatedly noted that morale inside the club went through a historic low during the cost-cutting phase, that several senior hires did not work out, and that the broader leadership structure, while more coherent than under the previous Glazer-only model, is still feeling its way through the implications of split ownership and operational authority.

For private equity and infrastructure investors, this is the most instructive part of the case. Minority deals with operational control are increasingly common in sports, partly because full takeovers in elite football are politically and financially difficult, and partly because sellers prefer to keep optionality. The Manchester United deal shows what happens when that structure is priced as if it were a controlling stake. The buyer carries operational risk, reputational risk, and execution risk, but does not have the unilateral authority to restructure the asset the way a majority owner could. The structure works as long as results trend in the right direction. The real test comes the next time they do not.

The next chapter: a two-billion-pound stadium with no clear financing path

The story is not over, and the most consequential chapter has barely started. Manchester United announced in March 2025 that they would build a new 100,000-seat stadium, designed by Foster + Partners, with an estimated cost of around two billion pounds. Ratcliffe described the project as eminently financeable. The reality, twelve months later, is that no funding has been secured. The club’s existing debt levels make traditional borrowing problematic, issuing new shares would dilute both the Glazers and INEOS, and bringing in external investors to take partial ownership of the stadium itself would complicate any future sale of the club. Lord Coe, who chairs the regeneration taskforce, travelled to New York last summer in search of potential investors, and the Old Trafford Regeneration Mayoral Development Corporation held its first meeting only recently. The signature tent-style canopy roof, which would add an estimated 200 million pounds to construction costs, may already be on the chopping block.

The stadium project crystallizes the underlying tension of the deal. Manchester United needs capital, and the existing ownership structure makes raising that capital structurally difficult. Any solution requires either further dilution, additional leverage on an already heavily indebted balance sheet, or a creative third-party arrangement that introduces yet another layer of governance complexity. None of these options are clean, and all of them will test the limits of the operational-control-without-ownership model that defined the original transaction. A top-three league finish helps the narrative, but it does not change the arithmetic of a two-billion-pound capex commitment.

What this deal teaches us about football M&A

The Ratcliffe deal will be studied for years, not because it is a failure, but because it is genuinely innovative and genuinely complicated at the same time. It demonstrated that elite football clubs can be acquired in pieces, with control rights decoupled from economic rights, in ways that would be considered unusual in most other industries. It also demonstrated that paying a premium valuation for a minority position is a difficult thesis to defend when the underlying financial structure deteriorates, when operational savings cannot offset revenue erosion, and when the next round of capex sits outside the original investment perimeter. The recent sporting recovery softens that critique, but it does not eliminate it.

For the next generation of investors looking at football assets, whether they come from private equity, sovereign wealth, or industrial wealth in the Ratcliffe mould, the lesson is straightforward. Football M&A is not about owning a trophy asset. It is about controlling the cash flows, the capex, and the governance with enough authority to drive a coherent long-term strategy. Anything less than that, no matter how elegantly structured, leaves the buyer carrying risk without the tools to manage it. Manchester United may yet complete their recovery, the new stadium may yet be built, and Ratcliffe’s stake may yet appreciate. But the deal will be remembered as the moment the football industry discovered that minority control is a powerful instrument when results cooperate, and a fragile one when they do not.