Football has never been bigger as a business. The biggest clubs are global brands worth billions, broadcasting deals stretch across every continent, and private equity firms, sovereign wealth funds, and industrial billionaires are all fighting to get a piece of the game. And yet, for all that financial gravity, one thing remains strangely true: almost no football club is listed on a stock market. The handful that are have mostly been poor investments, the kind that look exciting on paper and disappointing on a price chart. For an industry that loves to talk about growth, commercial revenue, and brand value, football has a remarkably bad relationship with public markets, and the reasons why tell you a lot about what kind of asset a football club actually is.

A short list, getting shorter

When you list the football clubs trading on public exchanges, the surprise is how short the list is. Manchester United sits on the New York Stock Exchange under the ticker MANU, valued at roughly 6.6 billion dollars and still one of the few major clubs with publicly traded shares. In Germany, Borussia Dortmund listed on the Frankfurt Stock Exchange in October 2000 and remains, as of 2025, the first and only Bundesliga club ever to go public. Italy contributes Juventus, Lazio, and AS Roma, all listed in Milan. Then come a scattering of clubs across smaller markets: Ajax in Amsterdam, Porto, Benfica, and Sporting in Lisbon, and a few Turkish giants like Fenerbahce and Galatasaray.

That is essentially the whole universe. A sport that generates tens of billions in annual revenue is represented on global stock markets by a list you can write on the back of a napkin. And the more interesting detail is that the list used to be longer. In England especially, going public was briefly fashionable in the 1990s, and clubs like Tottenham, Celtic, Sheffield United, Birmingham City, and Millwall all spent time as listed companies before quietly leaving the market again. The trend, in other words, has not been toward more football clubs joining public markets. It has been toward fewer.

The numbers do not lie

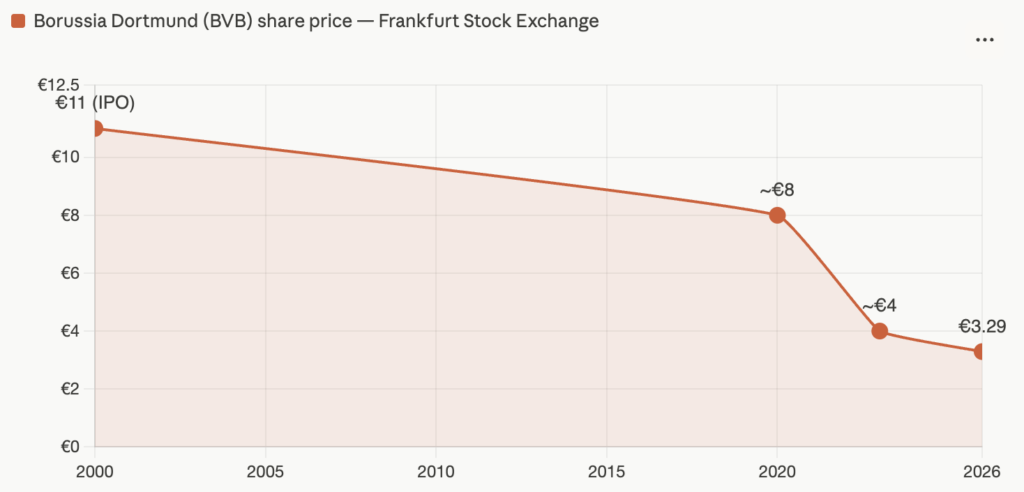

The reason owners and investors have cooled on the idea is not complicated. Football stocks have, with very few exceptions, been bad investments. Borussia Dortmund is a clear example. The stock launched at 11 euros at its IPO, has traded below 8 euros since 2020, fell below 4 euros in 2023, and now sits around 3.29 euros. This is a club that reaches the Champions League regularly, develops some of the best young talent in Europe, and was valued by Forbes at 2.05 billion dollars in 2025 with annual revenue of around 531 million euros. Strong brand, frustrating chart, as one analysis neatly put it.

Juventus tells a similar story. The stock traded at around 2 euros in June 2026, near the bottom of a 52-week range that stretched from 1.88 to 3.35 euros, and the club’s market capitalisation sat at roughly one billion dollars. For one of the most decorated and globally recognised clubs in the world, that is a humbling valuation, especially when you remember how much money has been poured into the squad over the years.

This is not bad luck or a run of poor management at one or two clubs. It is a pattern, and the academic research backs it up. A study by Baur and McKeating found that the majority of football clubs do not perform better in domestic or international competition after their IPO than before, that football stocks are generally poor performers, and that they are consistently outperformed by broader stock indices. The same research found something even more revealing about timing: clubs tend to go public when football valuations are already high, which means subsequent poor financial and on-pitch performance is almost baked in from the start. In plain terms, clubs float at the top of the cycle, and shareholders ride the disappointment down.

Why football breaks the public market model

To understand why this keeps happening, you have to think about what public markets actually reward, and then notice how badly football fits those expectations. Listed companies are supposed to deliver predictable, growing profits, return cash to shareholders, and reduce uncertainty over time. A football club does almost the opposite of all three.

Start with volatility. A club’s revenue and prestige depend heavily on sporting results, and sporting results are unpredictable by nature. A missed penalty, an injury to a key player, or a single bad season out of the Champions League can wipe out tens of millions in revenue and send the share price tumbling. No amount of commercial strategy fully insulates a club from the chaos of ninety minutes on a Saturday. Public markets hate that kind of uncertainty, and they price it in as risk.

Then there is the conflict at the heart of the whole model. A normal company exists to make a profit for its shareholders. A football club exists to win. Those two goals frequently pull in opposite directions, because winning usually means spending every available euro on players and wages rather than returning it to investors. When a club does well financially, fans expect that money to be reinvested in the squad, not paid out as dividends. The shareholder who bought in expecting a return is left holding a stock that, by design, prioritises trophies over yield.

This feeds into the tension between fans and investors. Many of the people who buy shares in a club are supporters who want a symbolic piece of something they love, not financial returns. Arsenal’s old share structure was a good example, where a single share cost a large sum and appealed far more to fans than to investors looking for profit. That makes for an unusual shareholder base and very thin trading, which only adds to the problem. With ownership concentrated and shares changing hands rarely, the market for football stocks is illiquid, prices move erratically, and the whole exercise starts to look less like a real capital market and more like a collection of sentimental certificates.

The exit trend

Given all of this, it is not surprising that the recent direction of travel has been clubs leaving public markets rather than joining them. The most telling case is Arsenal. In 2018, Stan Kroenke moved to take full control of the club, paying 550 million pounds for Alisher Usmanov’s 30 percent stake in a deal that valued Arsenal at 1.8 billion pounds, up from 731 million pounds when he first bid in 2011. He then took the club off the stock exchange and turned it into a private company. Kroenke’s reasoning was simple and revealing: he argued that private ownership would let the club move more quickly in pursuing its strategy, and pointed out that 18 of the 20 Premier League clubs were already privately owned.

Manchester United’s history points the same way, even if the club ended up back on the market. The Glazers delisted United in 2005 as part of their leveraged buyout, then relisted it on the New York Stock Exchange in 2012. The relisting was less a vote of confidence in the public model and more a way for the owners to raise cash and partially cash out while keeping firm control through a dual-class share structure. That is the modern attitude in a nutshell. Owners want the capital that markets can provide, but they do not want the scrutiny, the obligations, or the loss of control that comes with genuine public ownership. Private control, backed by private equity or sovereign wealth, has become the preferred model precisely because it removes the friction that public markets impose.

The exceptions that prove the rule

There are clubs that make the public model work, and they are instructive because of how deliberately they have adapted. Borussia Dortmund, despite its underwhelming share price, runs its business with a clear awareness of football’s volatility. The club deliberately diversifies its revenue through hotel bookings, travel services, and a stake in a medical rehabilitation centre, treating this as a conscious hedge against the unpredictability of sporting results. In other words, the one Bundesliga club brave enough to list has survived by building a business that behaves a little less like a football club and a little more like a normal company.

There are also moments when listing genuinely helps. The research suggests that lower-division clubs can clearly benefit from a stock market listing, because the capital raised has a much bigger marginal impact when revenues and wages are smaller. A flotation can also fund a specific, capital-heavy project, like a new stadium, which is part of the reason Lyon turned to public markets in France. And even when the share price disappoints, a listing can impose financial discipline and transparency that a club might otherwise lack. These are real benefits. They are just narrower and less glamorous than the growth story that usually gets told when a famous club decides to go public.

What this says about football as an asset

The deeper lesson is that a football club is not really a yield asset, and trying to wrap it in the structure of a publicly traded company has almost always been an awkward fit. People do not buy Manchester United or Juventus to receive a steady stream of dividends. They buy control of a football club because it is a trophy asset, a source of influence, prestige, and long-term capital appreciation that sits outside the normal logic of quarterly earnings. The value is real, but it does not behave the way public market investors want value to behave.

That is why the smart money has drifted toward private ownership, where a single owner or a tight group can absorb the volatility, prioritise winning over profit, and play a long game without a share price flashing red every time results dip. The public market was, for a brief period, football’s idea of how to grow up as a business. The verdict, written in three decades of disappointing charts and steady delistings, is that the game simply never belonged there.