A small Singapore pilot. A telco partnership. And a potential rewiring of the £6.78 billion revenue engine that sits at the top of world football.

On 26 February 2026, at the FT Business of Football Summit in London, Richard Masters announced something that sounded almost modest. The Premier League would launch its own streaming service, Premier League+, in a single market (Singapore) starting from the 2026/27 season, in partnership with local telco StarHub.

No big marketing campaign. No disruption to Sky Sports. No aggressive pricing war. Just a quiet six-year agreement in a city-state of 6 million people.

And yet this move, if it works, could reshape the economics of football more than any stadium redevelopment, transfer record, or UEFA regulation in the last decade. Because when you understand the scale of what currently flows through the broadcast model, the financial logic of what the Premier League is actually testing becomes impossible to ignore.

Argument 1: The £89 Million Per-Club Number Most People Miss

Start with the figure that already defines club finances at the top of English football.

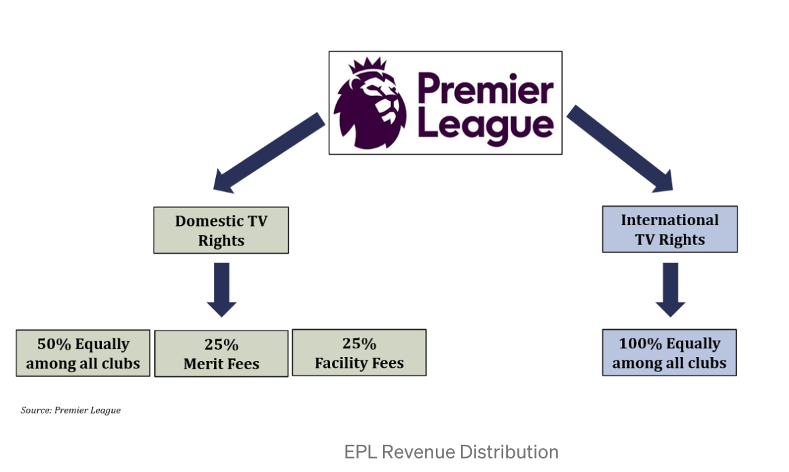

In 2024/25, every Premier League club received £89 million in equal-share broadcast distributions alone (£29.8 million from domestic TV rights and £59.2 million from international rights) regardless of where they finished in the table. Add £7.9 million from central commercial distributions and the equal-share floor rises to £96.9 million per club. Even Southampton, finishing rock bottom, banked £106.7 million in broadcast revenue. Champions Liverpool collected £174.9 million. In aggregate, the Premier League distributed £2.83 billion to its 20 clubs in one season.

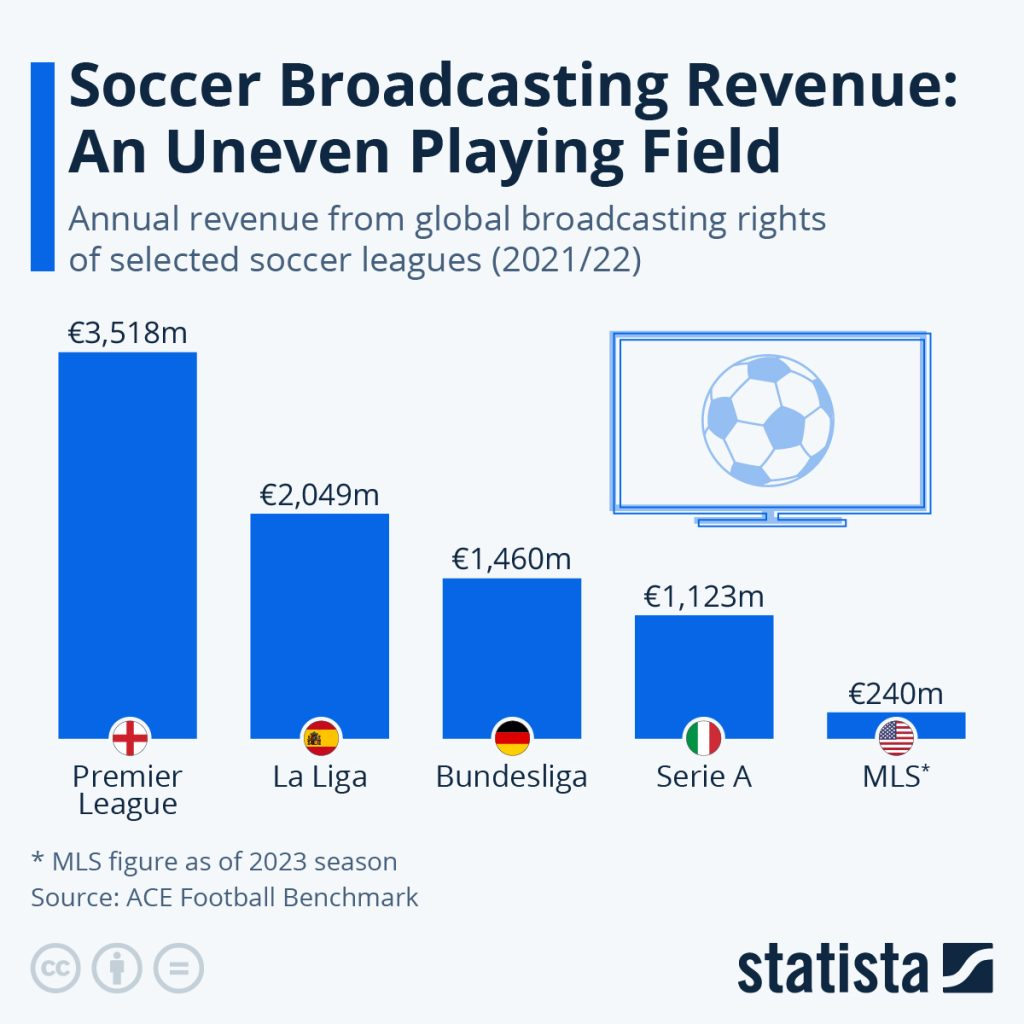

These numbers are the beating heart of the Premier League’s financial dominance. La Liga, the Bundesliga and Serie A combined generate less broadcast revenue than the Premier League alone.

But notice something important: £59.2 million of that equal share, two-thirds of it, comes from international broadcast rights. That is the exact portion Premier League+ is designed to start replacing. Not the domestic Sky Sports and TNT deals, which run safely through 2028/29. The foreign broadcaster cheques. The money currently paid by StarHub, NBC, beIN, DAZN and a hundred other licensees around the world, currently worth £6.5 billion over the 2025-2029 cycle.

If Premier League+ demonstrates that the league can extract more value per international viewer directly than it earns through licensing, the entire foundation of that £59.2 million per-club annual payment changes character. It stops being a rights-sale dividend. It becomes a subscriber-driven revenue stream, with different growth dynamics, different risks, and potentially a much higher ceiling.

Argument 2: The Margin That Currently Flows to Broadcasters

Every pound a Premier League club receives from international rights today is a pound that StarHub, NBC or beIN collected after building their own margin on top.

Broadcasters don’t buy rights at cost. They bid aggressively (NBC pays roughly £378 million annually for exclusive US rights, StarHub around $45 million (approximately £35 million) a year for Singapore) then monetise those rights through subscriptions, advertising, and ancillary products, capturing a substantial margin for themselves. That margin is the broadcaster’s reward for taking distribution risk, funding marketing, and owning the subscriber relationship.

Premier League+ is an attempt to capture that margin.

Consider the simplified arithmetic. In Singapore, StarHub currently pays around $45 million per year for Premier League rights. If the league’s direct-to-consumer service eventually generates, say, £60 million in gross subscriber revenue with £15 million in distribution and operating costs, the league nets £45 million. That is approximately 29% more than the current licensing model, before any cross-sell or advertising upside.

Now imagine that margin expansion replicated across ten international markets over the next decade. Even conservatively, that is hundreds of millions of pounds per year flowing directly into the central distribution pool, which is the pool Premier League clubs share from. An additional £200 million spread across 20 clubs is £10 million per club, per year, permanently. That is the difference between Brighton affording another first-team signing or not. It is the difference between Everton funding a new training ground or not. And it is a genuinely new revenue category that has never previously existed.

Argument 3: Subscriber Data Is the Real Balance-Sheet Asset

In the traditional model, the Premier League knew almost nothing about its fans. It knew how many rights packages it had sold and how much each was worth. The actual viewers, who they were, what they watched, when they churned, what they’d pay more for, lived on the broadcaster’s servers.

Premier League+ changes that overnight in Singapore. For the first time, the league will own first-party subscriber data on a live product. Who signs up, who renews, who cancels when their club drops out of Europe, who upgrades for match-day highlights.

The financial value of this is not abstract. Look at what streaming-era data did for Netflix, Spotify and Amazon Prime: it enabled pricing experimentation, tiered products, targeted advertising, and most importantly, content decisions driven by behaviour rather than intuition. For a football league, first-party subscriber data translates directly into higher commercial revenue through sponsorship propositions that can be quantitatively targeted, advertising inventory that can be sold at premium CPMs because it’s addressable, and dynamic pricing that can extract more value from high-intent customers without alienating price-sensitive ones.

At the club level, this matters because the Premier League’s central commercial revenues, currently £7.9 million per club, are still a fraction of what they could be if the league could demonstrably prove audience value to sponsors in the way that streaming platforms do. Subscriber data is the mechanism for that proof.

Argument 4: The Widening Gap With European Football

This is the argument that matters most for clubs outside the Premier League.

Ligue 1 has just launched Ligue 1+ after DAZN walked away from a €400 million-a-year broadcast contract. The French league’s direct-to-consumer experiment has been a rare bright spot, pulling in over one million subscribers in its first month and raising central media revenue projections to around €155 million ($166 million) for 2025/26, up from an initial €142 million forecast. That is still less than the broadcast equal share at a single Premier League club. Serie A’s total domestic broadcast pool sits around €900 million across 20 clubs. La Liga is grappling with plateauing rights valuations.

The existing gap is already brutal. Southampton, finishing 20th in England, earned more from broadcast revenue than Real Betis did for finishing 10th in La Liga.

Premier League+ threatens to widen that gap structurally. If the Premier League starts capturing margin directly from international consumers rather than licensing it to broadcasters, it adds a revenue lever that smaller leagues cannot easily replicate at scale. Direct-to-consumer economics only work when you have enough international fans willing to pay for your product on a standalone basis. The Premier League claims 1.87 billion fans globally. Ligue 1 does not have that. Serie A does not have that. That asymmetry, which currently sits dormant inside licensing structures, becomes directly monetisable in a direct-to-consumer model, and the clubs at the top of that league capture the benefit.

For the Juventuses, Lyons and Schalkes of European football, clubs already fighting structural debt problems caused by the revenue gap, Premier League+ is not just a Premier League story. It’s an acceleration of the force pushing them further behind.

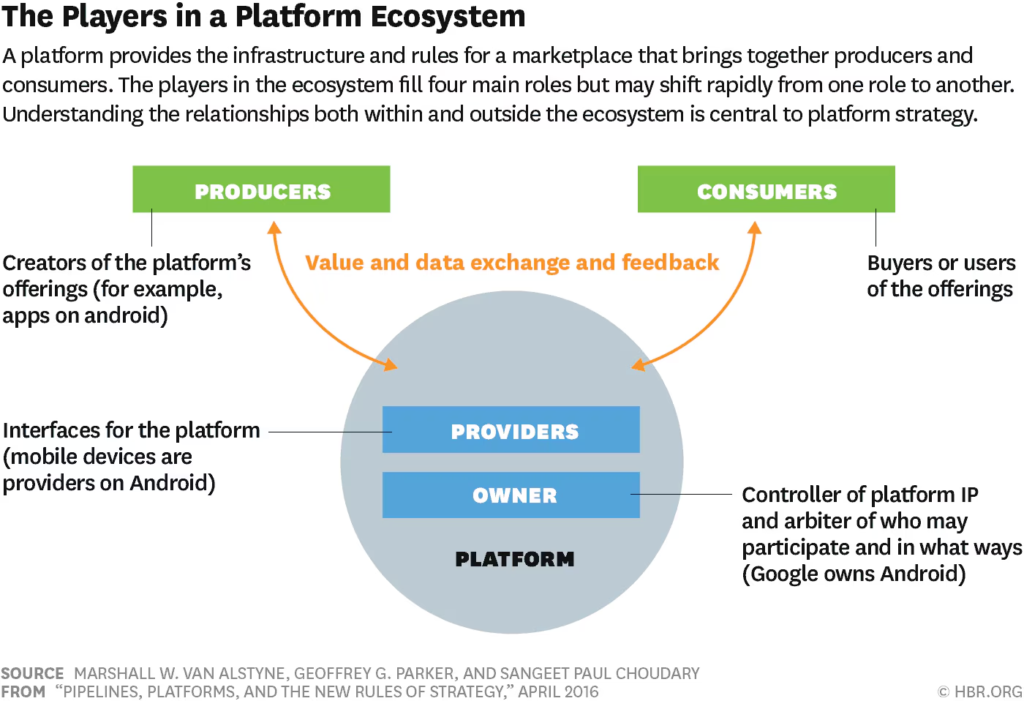

But Is It Actually a Platform?

Here’s where it’s worth pausing. Because despite all of the above, Premier League+ is not yet a platform. It is a transitional experiment that looks like one.

Forces of change: strong. Streaming disruption is eroding traditional broadcast-rights value. Fans demand flexible, unbundled access. Subscriber data is becoming the defining strategic asset in media.

Unmet customer need: strong. There is real demand for affordable Premier League access without a full pay-TV bundle, for a direct fan relationship without mediation, and for personalised content and scheduling flexibility.

Capabilities assembled: incomplete. Content IP is owned by the league, that part is solved. But local distribution sits with StarHub, an ally rather than an owned capability. And the subscriber data layer is a new capability being built for the first time.

The critical tension: owning the subscriber relationship end-to-end is what turns a pilot into a genuine platform. Partnering with StarHub delivers speed and reduced execution risk, but it also means the league does not yet fully control the customer. Billing, distribution, last-mile experience: StarHub holds it all. If the goal is a global DTC machine, that dependency eventually becomes a constraint.

The strategic takeaway: Singapore is a test market, not a launch market. The platform logic only succeeds if the league can standardise the model fast enough to prevent « distance costs » (the compounded friction of negotiating a new telco partner, a new billing system, and a new data integration in every new territory) from resetting with every new country.

The CashOnThePitch Verdict

Premier League+ is the most important football finance story of 2026, and it is being dramatically underpriced by the market.

On the surface: a modest pilot in a market worth $45 million a year. Beneath the surface: the first concrete test of whether a £2.83 billion annual distribution pool can be reorganised to capture broadcaster margin directly, and whether the international revenue line, currently worth £59.2 million per club per season, can be turned into a growth engine rather than a stable annuity.

If the pilot succeeds, every Premier League club is structurally richer within a decade. Every non-Premier League club is structurally poorer relative to them. And the broadcaster model that funded the modern game for 30 years quietly begins to expire.

That’s not a streaming product. That’s a rewiring of football’s entire revenue stack.

And it’s happening in Singapore first.